...

Understand how blockchain works and master the digital currency!

Deb Mukhuty

Deb Mukhuty

Learn about the core principles of blockchain, its benefits, challenges, and future to create a blockchain of your own!

Blockchain refers to a shared, immutable ledger that helps in the recording of transactions and the tracking of assets in a business network. It consists of all the transactions that take place across a peer-to-peer network. Blockchain increases the security, trust, traceability, and transparency of shared data across a business network.

Blockchain technology is frequently connected to cryptocurrency and is rapidly gaining popularity because it enables a secure and decentralized method of moving assets. The banking sectors focus exclusively on this technology as it can completely transform the current financial services.

This technology can be utilized to construct a distributed identity verification system. It also helps reduce fraud and identity theft by providing a tamper-proof and secure way of verifying identity. There are lots of applications of blockchain technology. Some examples include money transfer, financial exchange, insurance, real estate, voting, artist royalties, logistics and supply chain tracking, data storage, and non-fungible tokens.

Are you new to blockchain and want to master blockchain for beginners? Read on and learn how blockchain works step by step!

The core principles of blockchain technology include:

Decentralization: In blockchain, decentralization is the transfer of control and decision-making processes from a centralized unit, such as an individual or an organization, to a distributed network. This is in sharp contrast to centralization, where a central authority controls all the networks. By decentralizing the access to and management of resources in an application, fairer and greater services can be gained. Even though this process has some trade-offs, like lower transaction throughput, it is worth the service levels and the improved stability they produce.

Cryptographic security: Cryptography provides a way for secure communication in the presence of adversaries, which are malicious third parties. In blockchain, each new block connects to all the blocks ahead of it in a cryptographic chain in a way that it becomes nearly impossible to tamper with it. All the transactions within the blocks are agreed upon by a consensus mechanism, ensuring that each transaction is correct and true.

Distributed ledger technology: Distributed ledger technology is a platform that uses ledgers stored on separate and connected devices in a network. Because of this, the data and transactions are recorded identically in multiple locations. It ensures security and data accuracy. All the network participants with permission access can see the same information simultaneously, with full transparency. Distributed ledger technology speeds up transactional time, reduces operational inefficiencies, is automated, and functions 24/7 hours.

Consensus mechanisms: A consensus mechanism, in blockchain systems is a program that is used to achieve distributed agreement about the state of the ledger. It prevents unauthorized users from authenticating bad transactions. Reaching consensus is a vital part of how transactions are processed and settled. It is what keeps the decentralized networks secure.

Transparency and trust: Blockchain’s tamper-proof and transparent nature is the key to earning the trust of its participants. Without consensus from the majority of the network participants, every transaction that is recorded on blockchain cannot be altered retroactively. Moreover, blockchain has end-to-end encryption to keep away unauthorized activity and fraud.

Enhanced security: The decentralized nature of blockchain guarantees enhanced security against any type of cybercrime. This technology contributes to eliminating fraud as each and every transaction is verified and recorded on a public ledger. Also, another crucial security feature in blockchain, called cryptographic hashing, lets each block in the chain be uniquely linked to and identified with the previous block.

Reduced costs and efficiency: Implementing blockchain can reduce operating costs. Companies can decrease expenditures on transaction fees and exhaustive audits by removing intermediaries and streamlining processes. Blockchain also reduces costs by reducing paperwork and errors. It is also highly efficient as it strikes out intermediaries susceptible to manipulation and infiltration.

Scalability issues: In blockchain, scalability bottleneck problems lead to difficulty in functional extension and low-performance efficiency. Scalability issues make the validation of transactions tedious and very slow, with no scope to enlarge the block on a blockchain.

Energy consumption concerns: Many blockchains use a validation mechanism called 'proof-of-work.' This process uses a lot of computing power, which results in the consumption of a substantial amount of electricity. This requires a lot of energy and has led to concerns regarding carbon emissions.

Regulatory and legal challenges: Some of the regularity and legal challenges when creating a blockchain are:

Tax considerations

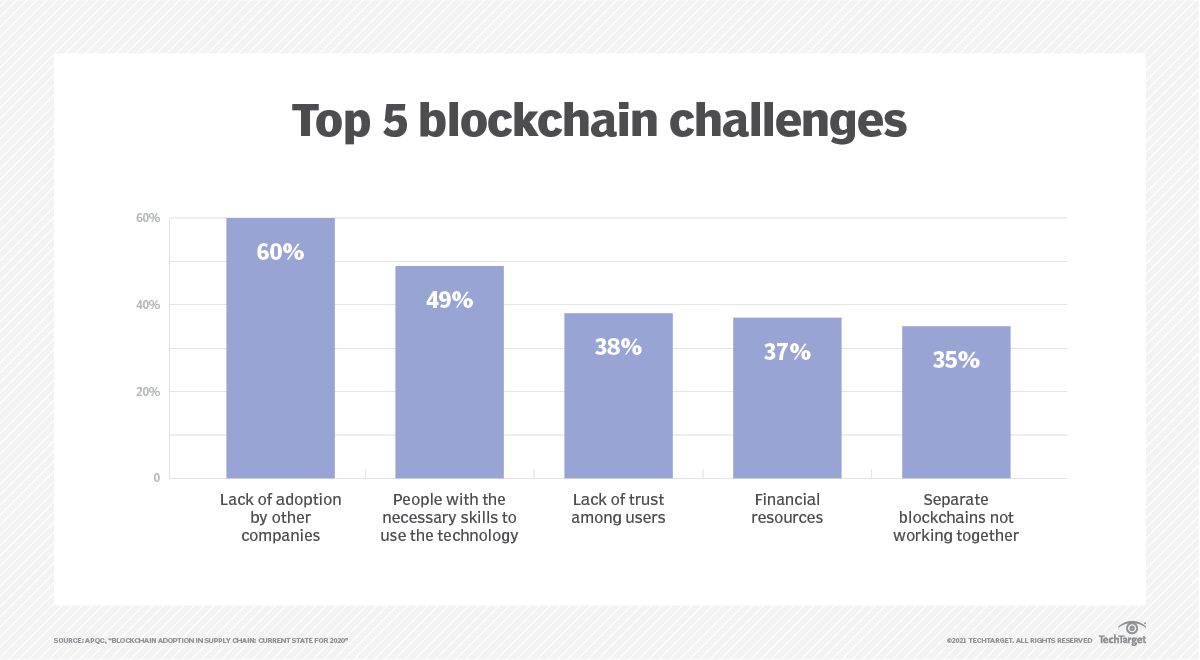

User education and adoption: User education and adoption issues in blockchain technology include skills gap, distrust among users, lack of financial resources, blockchain interoperability, slow development pace, and lack of regulation.

Source: TechTarget

Interoperability and integration: Blockchain interoperability refers to the capability of blockchains to communicate with other blockchains. It enables distinct blockchain networks to integrate and interact seamlessly so that data can be shared between chains. On the other hand, blockchain integration is a technology that creates an immutable record of transactions, which can be utilized to optimize business processes, maintain trust between stakeholders, and enhance security.

Emerging trends (e.g., NFTs, DeFi): Some of the emerging blockchain trends that are ready to shape the future of technology are:

Blockchain-as-a-Service (BaaS)

Growth of Decentralized Finance (DeFi)

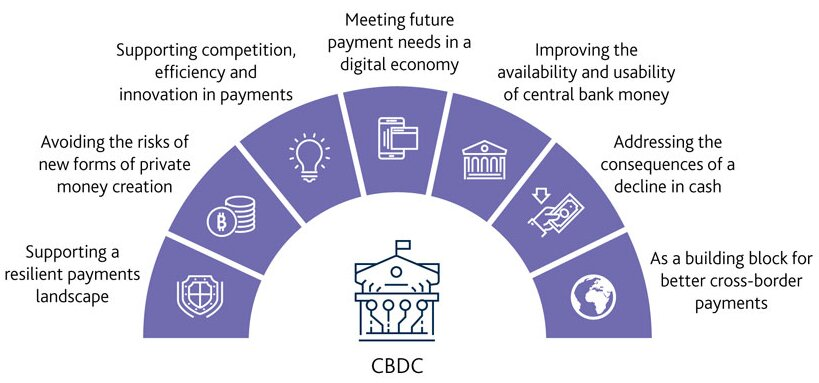

Central Bank Digital Currencies (CBDCs): Central Bank Digital Currency is an initiative of the Financial Infrastructure Transformation (FIT) Programme whose aim is to accelerate the digital transformation of the financial services sector. CBDC operates on a transparent and secure blockchain network. It uses blockchain technology to create an immutable record of every transaction.

Source: Sunya IAS

Learning resources and books: If you want to learn about blockchain technology and blockchain strategies, here are five books that you can consider reading:

Cryptoassets by Chris Burniske and Jack Tatar

Blockchain Revolution by Don and Alex Tapscott

The Book of Satoshi by Phil Champagne

The Basics of Bitcoins and Blockchains by Antony Lewis

The Blockchain Developer by Elad Elrom

Some other resources to learn about blockchain development are:

Crypto Zombies

Alchemy University

SPEEDRUN ETHEREUM

Buildspace

LearnWeb3

Creating a cryptocurrency wallet: A cryptocurrency wallet is an app that lets you store your private keys and receive, send, and spend digital money. You can create your cryptocurrency wallet by following a few basic steps. To create a Software Crypto Wallet, you need to:

Select a software wallet app

Download the wallet app to your phone or computer

Create an account

Transfer your assets.

To create a Hardware Wallet, you must:

Select the hardware you want to use

Purchase the hardware and install the required software

Transfer your cryptocurrency

Experimenting on Testnets: In blockchain technology, a testnet is an instance of a blockchain-powered by either the same or a newer version of the underlying software so that it can be used for experimentation without any risk to the real funds or the main chain. It enables a complete testing of a blockchain project, allowing developers to experiment and create the optimal launch model.

Since 2014, the world has realized that blockchains can be used for more than just cryptocurrency and financial transactions. With its trustworthiness, security, traceability of data, and transparency, blockchain is evolving rapidly. The global blockchain technology market is estimated to reach 1,235.71 billion U.S. dollars by 2030.

So, if you want to know more about blockchain and make use of its advantages, follow the instructions given in the article and capture your own space in its ever-evolving market!

What is your opinion on the growing market of blockchain technology? Let us know on Linkedin, Facebook & Twitter!

Deb Mukhuty is Lorem ipsum dolor sit, amet consectetur adipisicing elit. Illum consectetur quas nisi obcaecati. Qui ratione ab dicta similique ut consequatur at consequuntur, a laudantium sit nobis, neque provident sapiente sequi hic saepe facilis esse ipsa.